Get your FREE sample of the 100 Steps to Financial Independence Book here

After setting your goals to Financial Independence, the next part of your journey is to determine your current starting point. With those two things together, i.e. where you want to get to and where you currently are, it’ll be a lot easier to plan out how to achieve your goals.

Part 2: Define your Starting Point

One common obstacle to achieving financial independence is consumer debt. Most people have some type of debt they have to deal with and pay off, such as student loans, credit card debt, car loan and / or a mortgage. The first step in determining your starting point is to list all of your debts with their current outstanding amounts (i.e. what you still owe) and then total those amounts to get an overall amount.

While debts represent the negative side of a financial picture, most people also have a positive side: their assets or possessions that are worth something. This can include anything from a house to a savings or investment account as well as antique or art of a certain value. Do the same as what you did with your debts: list anything you own along with its estimated value and total those amounts.

With these two numbers you can now calculate your net worth: a very useful indicator of how healthy your personal financial situation is. Simply take the total value of all your assets, then subtract the total amount of debts you have to find your current net worth. Note that this might be a negative number!

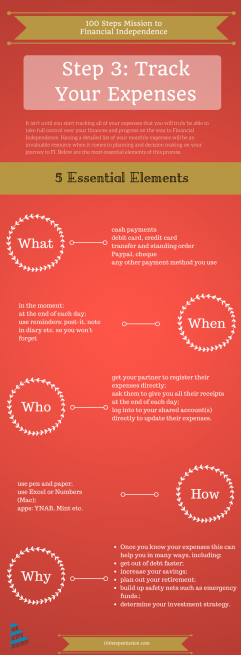

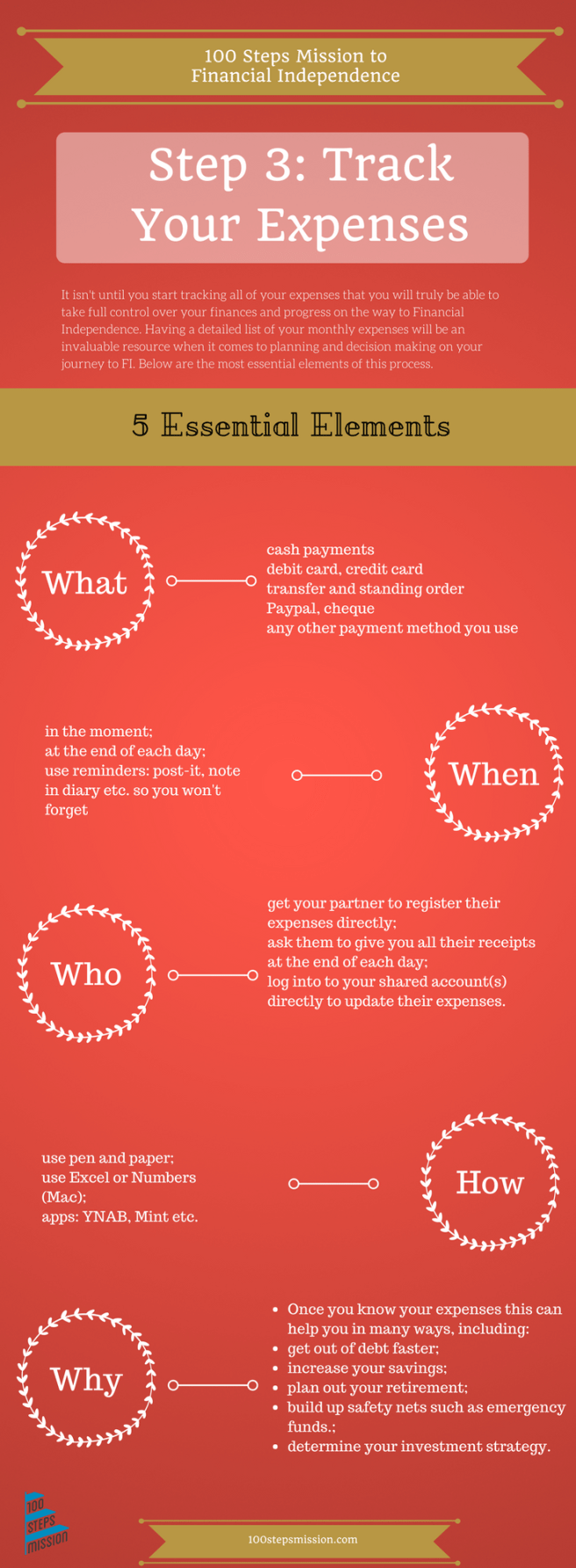

Lastly as part of determining your starting point, it’s a good idea to get a solid overview of your current expense patterns. Not only does this help to see where your money is going, it will also come in useful when you start setting goals later on in your journey for the various financial areas we’ll be looking at. Start logging your expenses on a daily basis to get a good idea of what you spend your money on.

Find some time today to look at the tasks above to complete to keep progressing on your path to Financial Independence!

The above is an adaptation of part 2 of the 10 parts in the guidebook to Financial Independence: 100 Steps to Financial Independence: The Definitive Roadmap to Achieving Your Financial Dreams where you can find more details as well as action plans and guidelines to each of the 10 parts. Available in both ebook and paperback format!

Coming up next: Part 3 of the Journey to Financial Independence!