Our next step of the 100 steps mission to financial independence is to set yourself a goal for what you would like your net worth to be in six months. This gives you an excellent target to work towards to during the mission. Although you’ll probably find that your net worth doesn’t change dramatically in this half a year, 6 months is a good time frame to start with as it is long enough to see substantial changes and the effects of goal setting, yet short enough not to forget about it or lose track.

You can set yourself a goal for your net worth by either stating a specific amount, or alternatively by setting a percentage by which to increase your income. If you set a specific amount as your target and keep that the same every six months, with time as your net worth increases and as it should become easier to achieve the same target, you might not be achieving as much as you could. Alternatively, if you set yourself a target of certain percentage increase it means that your net worth target increases more as your net worth itself increases.

In this 6th step, you are going to determine your overall financial starting point by calculating your net worth. I know the words “calculate” and “net worth” might be putting you off, but this step is a lot easier than it might sound, as we have already done all the preparation work in the last few steps by digging up financial statements and creating our assets and liabilities lists in step 4 and 5.

Your net worth basically indicates what would happen if you decided to sell all of your possessions and pay off all of your debts today: would you any have money left over or would you still be in debt? How much money would you have left over or how much money would you still owe? Your net worth is an easy sum of your total amount of assets minus your total amount of liabilities. Continue reading “Step 6: Calculate your Net Worth”→

Now we know exactly what our debts (or liabilities) are, in this step we are going to look at what our possessions (also known as assets) are. Assets add a positive value to our financial status: they are the things that we own and therefore add a positive value to our balance sheet.

Making an overview of all your assets, will not only allow you to know exactly how much you own at present, it also gives an insight into what you might be able to do in order to increase the number or value of your assets, thereby increasing your financial value.

Now that you’re happily (?) tracking away your expenses, which we know will take a while to keep doing before we have a solid, reliable list, we are going to continue with other steps we can take in the meantime. To start with, we are going to pull up an overview of any outstanding debts – also known as liabilities – you have. Sounds like fun? No I didn’t think so, thinking about your debts is usually not a lot of fun, but since your debts are probably also one of your biggest worries or financial strains anyway, we need to find out how bad (or not) the situation is to begin with.

Borrowing money is a relatively common thing in our current society and although it might sound like a great way to finance big purchases, the problem is that as long as you have debts, you are not only tied to paying back money all the time, you are furthermore consistently losing money. Borrowing money comes at a high price: the interest that you are charged can been enormous and in later steps we’ll look at how quickly this interest can add up to massive extra charges. Yet we seem to always be borrowing money these days, first to get through college, then to buy a car, a house, that fancy holiday and it becomes more and more of a habit to buy first and finance later. And kid yourself not: unless you are paying off your credit cards in full at the end of each month, the overdraft on any of these cards are loans too! Continue reading “Step 4: List your Debts”→

This post describes the details of tracking your expenses on your journey to Financial Independence. To see how I personally started tracking my money, check out the from level 2 to level 3 post: Tracking my expenses, which includes practical ideas on what, when and how to start this new habit.

Now that you have your goals clear of where you would like to get to financially, we are first going to look at what happens to your money and how you are spending it. Once you know what your current spending patterns are, you can evaluate whether they align with your financial goals and whether you need to set aside more or less money for your goals.

Obviously your spending changes from week to week and month to month as you don’t always need new clothes, a car that needs fixed and even your weekly shopping bill is different every time you go to the supermarket. Therefore, in order to find out where your money goes, you are going to track your spending. By registering your expenses you are furthermore becoming more conscious of spending your money, which is likely to result in a slight decrease in your expenditure in general. 🙂

There are various tracking options available. There is the good old notebook that you can carry around with you to register all your expenses in, but there are also (paid and free) online options and apps, such as YNAB (You Need a Budget), Mint and EveryDollar. You could also create your own spreadsheet in a programme such as Microsoft Excel. The advantage of the online programmes / apps is that they will allow you to plunk in any expense at the very moment that you are making a payment and some allow you to import your bank statement too. They can often give you reports depending on how you’ve set up categories, so have a look around and decide what you prefer and what you feel works best for you. That said, don’t use “having to find the best option” as an excuse not to start. If you don’t have time to investigate the options today, just start registering your expenses on paper and transfer them once you’ve made a decision on your definitive method of tracking.

Step 3 – Track your expenses – in detail

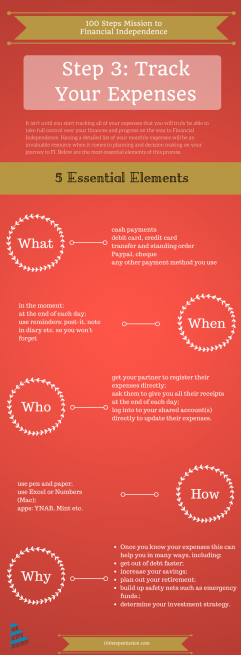

Starting today, keep track of everything that you spend, no matter how small or insignificant the expense might seem. This is not just cash, remember to also include any debit or credit card payments, standing orders and any other form of payment.

Record your expenses in one place, don’t worry about whether or not it is the perfect system and whether it is set up in the best way possible. The most important thing for now is to just start and then with time find out what system works for you.

When you get a chance, investigate alternatives to register your expenses, be that digital or in analogue format. Remember that if you want to use a digital expenses tracker on different devices, such as your computer, tablet and / or phone, you’ll want to make sure that it works on all of them and that any updates get synced automatically.

Settle for an option that you feel is easy to use and that fits in with what works for you. If you choose a system that you don’t feel motivated to use, you are unlikely to update it and you will most likely stop tracking your expenses after just a few days.

Log your expenses for at least three months, although it is a good habit to keep up in general even after these initial months, to see how your expense patterns change with time and to keep track of your money in general. Especially yearly expenses and emergency expenses might otherwise not become clear.

Add this step to a post-it, card, your mobile phone or journal, so you are reminded of your new task. You might also want to set yourself an alarm to remind you to write down your expenses twice a day to do it there and then, as if you leave it until the next day, you are likely to forget some of them.

If you ever forget to register an expense, don’t worry and most importantly: don’t give up on this entire step. Just accept that you forgot and continue again the next day. It requires quite a bit of time to get used to this new habit to keep a record of everything you spend, so it is likely you will forget now and again. That’s okay, just keep going!Obviously your spending changes from week to week and month to month as you don’t always need new clothes, a car that needs fixed and even your weekly shopping bill is different every time you go to the supermarket. Therefore, in order to find out where your money goes, you are going to track your spending. By registering your expenses you are furthermore becoming more conscious of spending your money, which is likely to result in a slight decrease in your expenditure in general. 🙂

To see how I personally put these ideas into action and set my own financial goals, check out the level 2 post: My Financial Objectives, which includes a free download of a worksheet to set your own financial targets!

One of the most important steps you can take towards becoming financially independent is making clear what your goals are. There is nothing more powerful than having a specific end objective that you are working towards to. Without stating your goal it is easy to give up after only a few initial attempts as you forget why you started this journey in the first place and because you have no way of measuring whether you are any closer to your target.

Numerous studies have furthermore shown that if you write down your goals you significantly increase your chances of ultimately achieving them, with some studies saying the likelihood of success increases by as much as 50% or more. So it is definitely worth stating your goals if you want to really achieve success on this mission! Continue reading “Step 2: Set Financial Goals”→

Step 1 of our 100 steps mission to financial independence

This post describes the hows of starting your mission to Financial Independence. To see how I personally put these ideas into action and started my own mission, check out the from level 0 to level 1 post: committing to Achieving Financial Independence, which includes a free download of a worksheet to get you started on this journey!

It’s exciting times as we are about to embark on our 100 steps mission to financial organization and independence! Or better said: as we have embarked on our mission, as this is our very first step! I hope you’re as eager to start and get your finances under control and set yourself up for successful money management as I am!

I’ll be here to help you along the way and to walk you through the 100 steps that will help you achieve your goal, doing just 1 step at the time. With every step you will feel more and more in control of your finances, as you organize yet another small part of your current, past or future finances. When we get to the end of our mission, you’ll be a finance ninja, managing your money responsibly and you should be well on your way to financial independence.

At times it may be a bit of a rocky ride, one in which you might get overwhelmed by information, feel you’re not getting nearer to your goal, and you might even feel yourself losing your motivation. All of this is totally normal, as if it were easy you’d already have your finances organized and wouldn’t need to join this mission! Don’t give up if this happens to you, it is (unfortunately) just part of the journey. A bit like learning to ride a bike and having to fall off a few times before finally being able to stay on longer and longer until you are a confident bike rider. That too took time and a don’t-give-up-attitude.

That said, we’ve all seen it happen to people who have great New Year’s resolutions: they start with a lot of enthusiasm, but then after a few weeks go back to smoking, eating too much or they stop hitting the gym. Let’s make sure that this won’t happen to you, even if you feel your motivation dipping at times!

So the very first, and also most important step on our journey is making a real commitment to our mission.

You might feel you’ve already committed by reading this blog or maybe you have been thinking about it for such a long time that you feel your mind is completely ready for the challenge. But it’s very important not to skip this step thinking you don’t need to do this if you’re currently über-motivated. You will (trust me!) at some point lose the desire to continue, so do yourself a favour and commit to your 100 steps mission to financial independence right now, now that your desire to do it is at its highest! (Remember those people with new year’s resolutions.. they were once too just as motivated as you are now). So let’s start with our very first action steps!

Step 1 – Commit to your mission – in detail:

We’re going to make a real commitment to our mission, so here are some ideas that you can use directly or get inspiration from to come up with your own ideas. Find what works for you and do it TODAY:

Write down your intention on a card or post-it, such as: “On a journey to financial independence”, “Getting my finances sorted once and for all!”, “On a mission to financial excellence”, “My 100 steps mission to financial independence”, or something that works for you. Stick the card somewhere where you will see it daily: in your wallet, in your diary, on the inside of the bathroom cabinet, in the car…Find a place that works for you and that reminds you of your new mission a few times a day.

Write your commitment down on your mobile phone and set daily reminders or alarms to look at your mission to remind you of it.

Change the screen saver or desktop of your computer with a message to remind you about it.

Find an accountability partner, be that your partner, a friend, a colleague or anybody else you can think of. Tell them that you are starting this mission and ask them to check in with you regularly to see how you’re doing and to hold you accountable.

Find a partner who is also willing to start this mission together with you. In that way you can check in together daily and make sure you don’t let each other down. You might even find several people willing to join and you can have your own WhatsApp group for daily accountability checks, or to help each other with the challenges.

Change your Facebook status to tell others you are starting this mission to make sure you will live up to it.

Write a short summary in your diary or special notebook, put a status update on your social media platforms, post a photo on Instagram that shows you starting or completing your latest step or even start blogging on every step or every day you have worked towards completing a step. Add the hashtag #100stepsmission to your social media posts so that other people can also find you and see how you’re doing.

Like the 100stepsmission Facebook page or follow 100stepsmission on Twitter to get frequent inspiration and find other people on the same mission.

Write an affirmation that you read out every morning and/or evening. An affirmation would be slightly longer than the commitment we wrote above, and could read: “I am committing to getting my finances in order, so that I know I am using my money in the best way possible for both the present as well as the future. Despite the fact that I have neglected my finances for many years and that I have substantial debts or money leaks, I know I am capable of getting back on track and improving my financial status and organization in order to become financially independent”. Make it part of your morning or evening routine to read out the affirmation and you’ll find that with time, you will really start to believe in it and it will help you keep your motivation up and get to your end goal.

As you can see there are many different ways in which to commit to your mission, find out what works best for you: getting other people involved, having a digital or paper log or reminder, using social media and the internet or anything else. Do what works for you and know that if you truly want to get to an organized financial life, there is no going back from here! So pick one or more of the ideas above or add your own and put it in place right now! Remember you’ve already jumped on the ride and got to the first stop, so let’s just fasten our seatbelt and hold on tight as we continue the journey. Oh, and try and enjoy it!

To see how I personally put these ideas into action and started my own mission, check out the from level 0 to level 1 post: committing to my mission, which includes a free download of a worksheet to get you started on this journey!