This post describes how I implemented step 2 of the mission to Financial Independence. To read more about how you can set your own financial goals, please refer to step 2: Set Financial Goals.

This post describes how I implemented step 2 of the mission to Financial Independence. To read more about how you can set your own financial goals, please refer to step 2: Set Financial Goals.

After making a commitment to achieve Financial Independence, the next level up is setting financial objectives. I wanted to set clear financial objectives that, although I was aware might still change later on in this mission when I dive a little deeper into different financial topics, would be my main anchors and most important outcomes of my journey.

At the start of my own mission to Financial Independence I identified to following objectives I wanted to achieve:

- Set aside money on a monthly basis.

This is an important one for me as I am aware that I should be setting aside money for my future. I want to make sure that I add to my monthly savings regularly to have separate savings to rely on when I become Financially Independent.

Added to that I also wanted to set aside a fixed amount each month for various short term goals so that when the time comes to make a purchase I not only have money set aside but also know how much I can spend on it. This includes a yearly fund for (Christmas) presents, flights (I don’t live in my home country but luckily living in Europe it is easy for me to go back and see my friends and family from home relatively easily, but I do of course need money to buy flights!) and medical expenses.

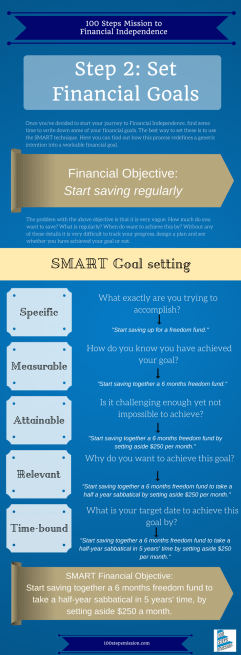

Using the SMART goal setting method (see infographic further up), this would translate into: “Build up a 6 months freedom fund by January 2023 in case I end up without an income to cover my expenses during half a year, by setting aside €150 per month.” And the second goal: “Set aside €100 per month for specific targets including flights, presents and medical expenses to be able to use whenever needed.”

* If you want to find out more about setting financial goals using the SMART technique, put your email below to get a free worksheet you can instantly print and use!*

- Plan how to become debt free

I have a (relatively small) student loan as well as a mortgage and whilst there are people who say you should pay off all debt as soon as possible, others are more cautious, bringing in arguments about interest rates, rate of return and inflation. All things that I couldn’t put together into a big picture or plan to know whether or not it was wise to pay of my debt as quickly as possible or not, as I didn’t know what these things meant nor how to use them to make a decision. As part of my financial journey I wanted to be able to decide if and how to pay off my debt as soon as possible based on knowledge I’d hoped to gather during this journey.

The SMART goal was therefore: “Know by May whether I should accelerate my debt payments, by understanding how inflation, interest rates and returns affect this decision. If I decide to pay down my debt aggressively, have a set plan to put into place by June.”

- Understand my pension provision

Admittedly I am still many years away from retiring (I’m in my 30s), but I didn’t feel comfortable not knowing anything about my pension and what that would look like. There are many stories going around that by the time my generation retires, our (state) pensions will no longer exist as they will have become too expensive to sustain. Not a great prospect so I decided I had to become proactive and learn what my own exact pension situation currently looks like and whether I needed to take steps to build in an extra safety net.

In SMART terms this would be: “By July I want to understand my own pension provisions projections I am entitled to and have a set plan to put into place starting that month if I decide to increase my pension contributions via a private pension plan.”

- Learn about investing

I never learned anything about investing and had no idea what shares and portfolios were when I set out on this mission. When people said they were investing part of me could only think that all those people were just bound to lose all their money soon, yet another part of me kept wondering why so many people were investing. Surely something must be attracting them into the market? Was there after all a way to make money on the stock market without a guaranteed financial disaster looming over? I wanted to learn about investing so that I could make an informed decision as to whether or not I wanted to start putting in some money too.

The SMART version was: “Understand what investing is and how it might apply to me personally. Decide whether to invest or not by August and have a plan to put into place by September if I decide to start investing.”

These were my four main objectives before I set out on my 100 steps mission. As you might understand I added in a lot of other objectives along the way and also modified some of the above, but knowing what I wanted to get out of this journey greatly helped me stay focussed and motivated. To read up more about setting financial goals, read the broken down explanation of step 2.

Grab your free worksheet to start setting your own Financial Goals here by leaving your email address below.

Let me know about your own goals below or on your favourite social media!