In step 18 we looked at starting a weekly finance review and what to focus on during that weekly half an hour, to ensure you stay on track for that month’s spending, bills and goals.

Today we are going to take this one step further, by starting a monthly finance review, in addition to your weekly review. Whereas the weekly review is incredibly useful to ensure you achieve your monthly goals, the monthly review helps you to achieve your longer term goals that you set out to achieve, such as becoming debt free, getting to a certain net worth or saving a specific amount of money. It is the moment to plan and look ahead a little further and to readjust your goals and spending patterns.

During most months you can probably combine every fourth weekly review with your monthly review, although for your monthly analysis you will need to set aside more time, as you are analysing the entire past month and also looking further ahead. I recommend scheduling in roughly 2 hours every month to complete this step. Continue reading “Step 25: Start a Monthly Finance Review”→

From the previous step you are now up to speed about the positive effect of extra payments on outstanding debts. That leads us to the current step: start paying off a debt. You might think you are already paying off a debt, or several of your debts, but the point here is that you are going to pay off a debt faster by making higher monthly contributions than the minimum required.

When you pay off a debt faster than scheduled, a few amazing things happen:

You end up paying less interest, resulting in a lower amount of money paid back overall;

It takes less time to pay back the loan, meaning you can tick it off your list a lot sooner;

Psychologically it is a great relief to have paid off a debt: one less thing to worry about;

It increases your motivation by showing you that you can achieve your goals;

And here’s a great thing: once you’ve paid off a debt, that monthly amount you poured into this debt suddenly becomes available, which you can then use in its entirety to pay off another debt, meaning it keeps up that momentum!

After some rather depressing news to do with debt and interest, it is again time for some uplifting information. In this step we are going to look at how powerful it can be to put extra money towards paying off a loan and how much it reduces not just the time spent on paying back the money, but also the total amount paid back.

This information will hopefully inspire you to find ways of making extra payments towards reducing your debts. As even if they are small extra payments, in the long run, thanks to that friend of ours called compound interest, it will have a huge effect.

Let’s go back to the same example as the one I used in step 21 to illustrate how credit cards work, in which we looked at an outstanding debt of $1000, at a 1,5% monthly interest rate and a payback rate of 3% with a minimum of $10. But this time you make an effort each month to pay the minimum amount (3% of the outstanding debt) and an EXTRA $25 on top of the minimum amount. Let’s see how this works out. Continue reading “Step 22: The impact of extra debt payments”→

It’s time to start looking at an area of your finances that makes many people nervous, scared and / or depressed, leaving them ignoring rather than analyzing and planning how to deal with that very same area: debts.

Yet in order to become financially independent and in total control of your finances, it is important to understand how debts work and how even seemingly small debts or amounts can make a tremendous difference to your long-term finances.

In step 4, you listed all of your debts, so you should have a good idea of how much debt you have and how much you are paying towards amortizing these loans. In this current step we are going to look at the effects of debt and how much extra you end up paying on any long-term debts. Continue reading “Step 21: Stop accumulating debt”→

You have probably heard about compound interest, and might even feel you understand the notion of compound interest quite well, but since it is the key concept in some of the next steps and because the impact of compound interest over time might be far bigger than you realize, this entire step is dedicated to looking at how compound interest works.

In finance compound interest is one of the most powerful factors at work that by using time as it catalyst, can do one of two things:

keeping you poor by losing money on outstanding debts

making you richer by making more money with the money you already have

No matter how organized you are and how carefully you have planned and budgeted for the next month, there will always be surprises that come up and hit you financially at unexpected and often inconvenient moments: a car maintenance or fix that you hadn’t planned for, a plumbing issue that needs immediate attention, a sudden vet bill for one of your pets or your washing machine that suddenly breaks down. I am sure you can think of many occasions and examples that could suddenly happen and throw you off-track.

If you don’t expect an expense to come up, often times you won’t have the money available, and you will either be forced to borrow money, eat into your savings or cut out money elsewhere.

In this step you are going to set up and build an emergency fund, in which you have a certain amount of money put away that you can use in case of these unforseen but needed expenses that come up. In that way you don’t need to worry about scraping the money together, you can just pay the bill and get on with your life. A good amount to aim for is generally $1000 or the equivalent in your currency. Whenever you take money out of this account, you aim to get it back up to the $1000 as soon as possible afterwards. Continue reading “Step 16: Start an Emergency Fund”→

By now you have (hopefully!) been tracking your expenses for a while so you should have a reasonably good idea of your spending. Ideally you would have at least 1 month’s worth of data to look at, if you have more than a month that’s even better. In the next few steps we will be looking at your expenses in detail to get a better idea of where your money is going, how much you spend on various categories and most importantly, whether this spending pattern is aligned with the way you WANT your money to be spent.

The first action step will be identifying the different areas that you are spending your money on by categorizing various expenses into groups, which will allow us to analyze in which areas of your life there is a potential to save more (or less) money. Continue reading “Step 8: Categorize your expenses”→

In this 6th step, you are going to determine your overall financial starting point by calculating your net worth. I know the words “calculate” and “net worth” might be putting you off, but this step is a lot easier than it might sound, as we have already done all the preparation work in the last few steps by digging up financial statements and creating our assets and liabilities lists in step 4 and 5.

Your net worth basically indicates what would happen if you decided to sell all of your possessions and pay off all of your debts today: would you any have money left over or would you still be in debt? How much money would you have left over or how much money would you still owe? Your net worth is an easy sum of your total amount of assets minus your total amount of liabilities. Continue reading “Step 6: Calculate your Net Worth”→

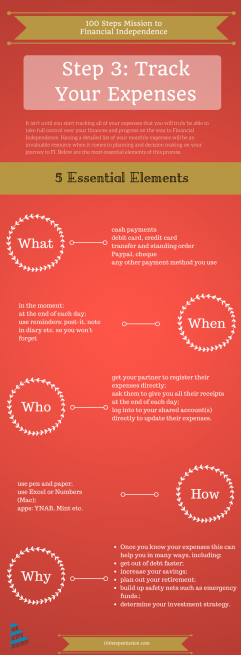

This post describes the details of tracking your expenses on your journey to Financial Independence. To see how I personally started tracking my money, check out the from level 2 to level 3 post: Tracking my expenses, which includes practical ideas on what, when and how to start this new habit.

Now that you have your goals clear of where you would like to get to financially, we are first going to look at what happens to your money and how you are spending it. Once you know what your current spending patterns are, you can evaluate whether they align with your financial goals and whether you need to set aside more or less money for your goals.

Obviously your spending changes from week to week and month to month as you don’t always need new clothes, a car that needs fixed and even your weekly shopping bill is different every time you go to the supermarket. Therefore, in order to find out where your money goes, you are going to track your spending. By registering your expenses you are furthermore becoming more conscious of spending your money, which is likely to result in a slight decrease in your expenditure in general. 🙂

There are various tracking options available. There is the good old notebook that you can carry around with you to register all your expenses in, but there are also (paid and free) online options and apps, such as YNAB (You Need a Budget), Mint and EveryDollar. You could also create your own spreadsheet in a programme such as Microsoft Excel. The advantage of the online programmes / apps is that they will allow you to plunk in any expense at the very moment that you are making a payment and some allow you to import your bank statement too. They can often give you reports depending on how you’ve set up categories, so have a look around and decide what you prefer and what you feel works best for you. That said, don’t use “having to find the best option” as an excuse not to start. If you don’t have time to investigate the options today, just start registering your expenses on paper and transfer them once you’ve made a decision on your definitive method of tracking.

Step 3 – Track your expenses – in detail

Starting today, keep track of everything that you spend, no matter how small or insignificant the expense might seem. This is not just cash, remember to also include any debit or credit card payments, standing orders and any other form of payment.

Record your expenses in one place, don’t worry about whether or not it is the perfect system and whether it is set up in the best way possible. The most important thing for now is to just start and then with time find out what system works for you.

When you get a chance, investigate alternatives to register your expenses, be that digital or in analogue format. Remember that if you want to use a digital expenses tracker on different devices, such as your computer, tablet and / or phone, you’ll want to make sure that it works on all of them and that any updates get synced automatically.

Settle for an option that you feel is easy to use and that fits in with what works for you. If you choose a system that you don’t feel motivated to use, you are unlikely to update it and you will most likely stop tracking your expenses after just a few days.

Log your expenses for at least three months, although it is a good habit to keep up in general even after these initial months, to see how your expense patterns change with time and to keep track of your money in general. Especially yearly expenses and emergency expenses might otherwise not become clear.

Add this step to a post-it, card, your mobile phone or journal, so you are reminded of your new task. You might also want to set yourself an alarm to remind you to write down your expenses twice a day to do it there and then, as if you leave it until the next day, you are likely to forget some of them.

If you ever forget to register an expense, don’t worry and most importantly: don’t give up on this entire step. Just accept that you forgot and continue again the next day. It requires quite a bit of time to get used to this new habit to keep a record of everything you spend, so it is likely you will forget now and again. That’s okay, just keep going!Obviously your spending changes from week to week and month to month as you don’t always need new clothes, a car that needs fixed and even your weekly shopping bill is different every time you go to the supermarket. Therefore, in order to find out where your money goes, you are going to track your spending. By registering your expenses you are furthermore becoming more conscious of spending your money, which is likely to result in a slight decrease in your expenditure in general. 🙂

To see how I personally put these ideas into action and set my own financial goals, check out the level 2 post: My Financial Objectives, which includes a free download of a worksheet to set your own financial targets!

One of the most important steps you can take towards becoming financially independent is making clear what your goals are. There is nothing more powerful than having a specific end objective that you are working towards to. Without stating your goal it is easy to give up after only a few initial attempts as you forget why you started this journey in the first place and because you have no way of measuring whether you are any closer to your target.

Numerous studies have furthermore shown that if you write down your goals you significantly increase your chances of ultimately achieving them, with some studies saying the likelihood of success increases by as much as 50% or more. So it is definitely worth stating your goals if you want to really achieve success on this mission! Continue reading “Step 2: Set Financial Goals”→